By Arihant Paigwar

An article in Nature Ecology & Evolution identifies conservation abandonment as a significant and largely overlooked policy area that hinders global conservation efforts. According to the paper “Conservation abandonment is a policy blind spot,” the widespread failure to implement conservation promises puts large international goals, such as the Kunming-Montreal Global Biodiversity Framework‘s aim to protect 30% of the land and oceans by 2030 at risk.

After their paper conceptualises conservation abandonment as a failure combination, the authors first depict the failure of regimes to perform conservation actions even after the signing of the agreements, resulting in “paper parks” that are only a term in documentation and have not been truly protected. Secondly, among the changes in the natural world, there is one called Protected Area Downgrading, Downsizing, or Degazettement (PADDD), which describes the legal court’s decision to cancel or reduce the administration of the area.

In their analysis of 3,749 PADDD cases in 73 countries between 1892 and 2018, they discovered that the protective statuses were lessened or removed over an area equivalent to the size of Greenland. One of the most important discoveries among their different findings was the strong relationship (directly linked to two-thirds) between the rollbacks and the performance of industrial-scale resource exploitation, such as mining, oil drilling, and large infrastructure projects.

The costs might be expected to rise over $540 billion by 2030, while the present global conservation effort is very conservatively estimated to be $87 billion per year and may exceed $200 billion depending on what is included. But Matthew Clark, a postdoctoral researcher at the University of Sydney, thinks that “No one can say how long these programs are going to last, but we certainly don’t have much of a line of sight.”

Studies also reveal that at least one out of every three conservation projects is abandoned within two years following the implementation. Clark adds that “This blind spot may very well signal the progress at COP type of events as real ecological recovery takes decades.” One of the biggest threats that have led to this situation of non-achievement of environmental goals is the lack of accountability and sustained effort.

The abandonment of conservation has been gaining momentum all over the globe. For example, the people of Chile were initially allocated 22% of the Territorial Use Rights in Fisheries, which, however, were later withdrawn. Specialists estimated that a portion of conservation-related community organizations in the southern and eastern regions of Africa which after that abandoned the management of their areas or changed their boundaries and regulations. Even “Other Effective Area-Based Conservation Measures” (OECM), which are recognized by GBF, are going through the change process. Two countries, Canada and Morocco, have together removed seven OECMs that cover over 2,400 square kilometres, and a vast maritime OECM has been authorized for exploratory oil drilling.

According to this report, abandonment dominates most of the regions with land use under heavy pressure and a decline in external funds. Society and culture changes, like secularization leading to less conservation of the holy natural sites, also affect the trend. Moreover, the paper identifies economic and political changes as the greatest risks. After the US government cut $365 million in international conservation assistance, it removed legal protections from ecologically vital areas like the Pacific Islands Heritage Marine National Monument and all 18 of California’s national forests in February 2025, the paper states. Europe right-wing populist parties, e.g., several of them, have been opposing the EU’s Green Deal whereas environmental rollbacks in Brazil under Jair Bolsonaro’s presidency (2019–2023) have led to the global conservation movement’s decline getting faster. The authors argue that if the issue of conservation abandonment is not addressed, it will be a substantial obstacle to the means of reducing biodiversity loss and meeting the global warming 1.5 C target.

Seven countries are getting a timely boost to make farming friendlier to nature. Backed by $5.8 million from the Kunming Biodiversity Fund, alongside the UN’s food agency, these projects aim at farm improvements, ecological protection, and invasive species management; all contributing to the biodiversity direction the Kunming–Montreal goals for 2030 produced.

What the funding enhances

This funding concentrates on practical and rapid-moving work, visible and tangible in communities. Connections between national biodiversity plans and practice in fields, borders, and water are relevant, supporting policies that lead to better practices on the ground.

Country highlights

Why this is important now

During these projects, we will able demonstrate how goals of a larger order are made more accessible through the synthesis and production of smaller, actionable steps with things like healthier soil, safer borders, cleaner water, and healthier communities in a more general sense. In fact, this is one of the most important steps, demonstrating that smaller, more specific grants can leverage larger grants better, and help countries accomplish their biodiversity goals by 2030. Even the FAO has shown the real evidence that nature friendly agriculture means a threefold win- better biodiversity, more diverse diet, and more tangible climate benefits that communities can use as a foundation.

By Arihant Paigwar

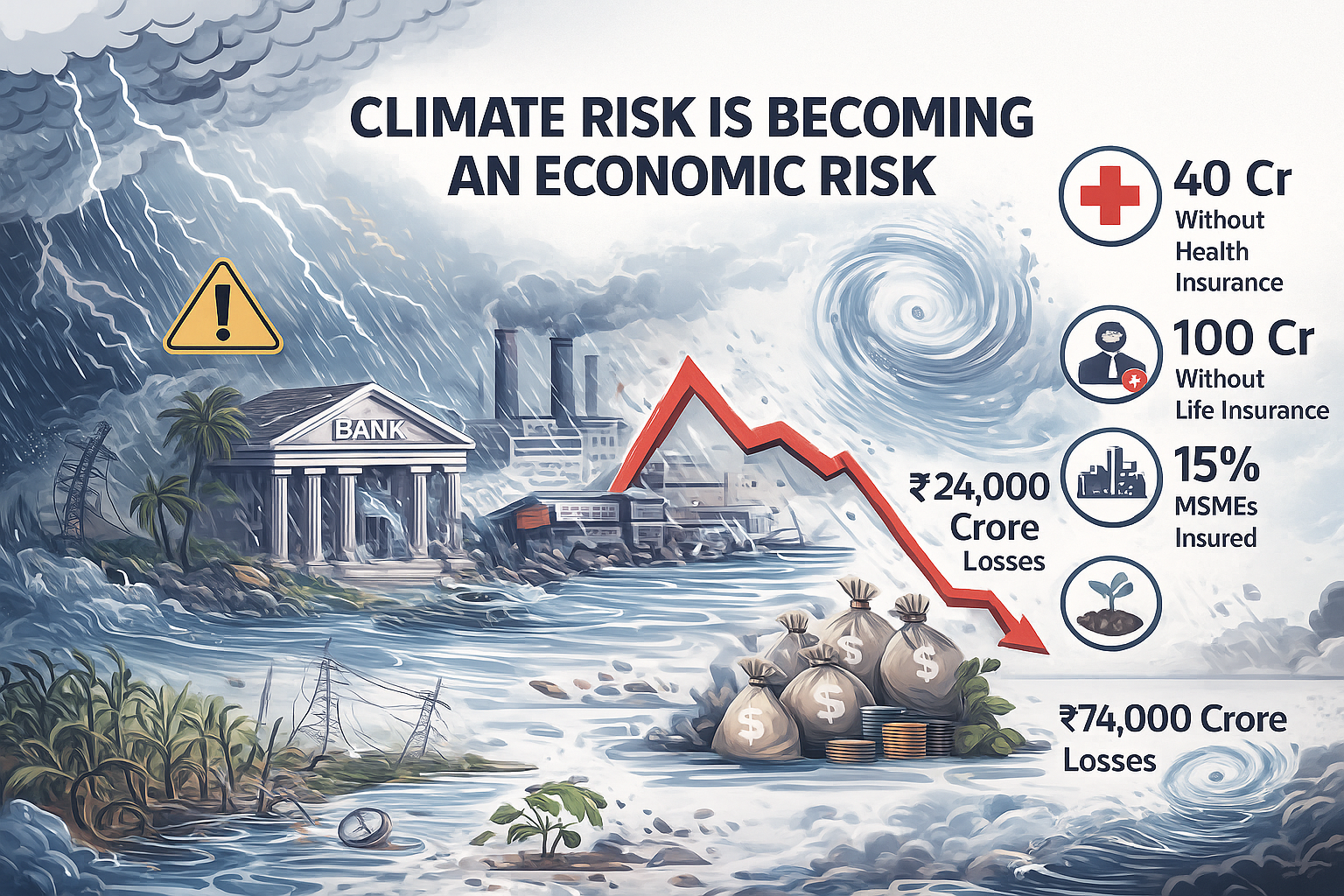

The increasing volatility and intensity of weather events, such as the October storms over the Bay of Bengal and the Arabian Sea, have a very powerful message for India: climate risk has turned into economic risk without any doubt. Such events as Cyclone Montha, which hit near Kakinada with winds of about 110 km/h, tell us that the weather is changing drastically and that our everyday life is getting more and more fragile. This kind of instability is a part of a worldwide trend, which is well exemplified by the very catastrophic events like a Category 5 Hurricane Melissa that was estimated to cause losses of $6.5 billion in the Atlantic. It acts as a warning not only for the financial effects of global warming but also for the consequences of human activities that are still going on without any control.

The consequences of climate volatility in India are manifold. It affects human lives, infrastructure, and even the money system. Just this year, during the monsoon season from June to September, irregular rains, floods, and landslides have killed more than 1,500 people, and the losses have been estimated to exceed ₹24,000 crore. The extreme rainfall that has been 27% higher than the Long-Period Average by mid-October has led to the destruction of the essential infrastructures like roads, bridges, schools, hospitals, and power lines in different states. The country is also exposed to major disruptions in various sectors, including agriculture, manufacturing, mining, and tourism. Therefore, the monsoon’s behaviour has transitioned from being a natural phenomenon to an important economic variable that has the power to change growth, employment, and fiscal stability.

As losses are rising to a great extent, the first and foremost question that a policymaker should ask himself/herself would be: where is the most significant protection gap? Although insurance is a very good tool for dealing with uncertainties, the majority of India’s people and economic activities have not been insured or have been only partly insured, which means that the losses are most of the time borne by individuals and enterprises who do not have any safety net. The figures disclose the extent of this exposure to risk: almost 40 crore citizens do not have health insurance, about 100 crore citizens are without life insurance, less than 15% of MSMEs have sufficient insurance, and roughly 70% of the gross cropped area is without any protection. In order to close this gap, India is taking the first steps towards climate-linked and parametric insurance models. These instruments are intended to facilitate automatic compensation when the weather conditions set in advance, for example, the intensity of rainfall or the speed of wind, are violated. These mechanisms aim to make the process of coverage faster, data-driven, and less difficult for the most vulnerable sectors, thus constituting a necessary advancement in the transition toward climate risk financing that has the capacity to absorb shocks at scale.

As climate volatility is becoming a matter of everyday life, India has to change its disaster response strategy from a focus on reactive relief efforts–what happens after the damage—to preventive planning and risk-building. The development of a country should not be judged only by indicators like GDP or production output, but also by the level of a society’s resilience–the ability to withstand shocks without losing its flow of life. Natural disasters, in the end, bring to light not only human weakness but also the power to adjust. Every storm that has been overcome is a kind of exam of how the protective systems, the responsive communities, and the collective will to rebuild stronger are at work. Hence, real growth is more about foresight than recovery rates.

By Prerna Singh

The festival season may have passed sometime back, but it left teaching us new lessons in green tech. This started with a calm shift under the bright lights of Dussehra in Ayodhya. Devotees carried prasad in neat boxes and drank from regular-looking water bottles. They may have looked ordinary, but they were not all made from sugarcane. Not sugarcane juice: a new product known as PLA the plant-based plastic that degrades safely in composting situations. It was a mundane example with a loud message: India can respect tradition, without the burden of plastic waste.

A moment like this does not just happen. Balrampur Chini Mills (BCML) was behind it. They did not simply deliver the prasad packaging for the festival, they built a model. Their Balrampur Bioyug brand made both the prasad containers and water bottles from sugarcane PLA, which was certified to IS 17088 standards even the cap was compostable. The effort fell well within the cadence of Swachhata Hi Seva 2025. Tradition transformed into a clean, modern, sacred-sustainability story of responsibility. And the effort to partner MSME converters based in the south and the west meant that small manufacturers were now included in that story.

However, the essence of this shift goes beyond only one event. BCML is building India’s first fully integrated “sugar-to-PLA” plant, where sugarcane becomes polymer in one continuous chain using renewable energy. It will have a projected capacity of up to 80,000 tonnes a year. This is sufficient production to move from pilot scale to mainstream and achieve cost reductions over time. Currently, PLA costs nearly twice as much as PET. In practice, it is about 1.5 times more due to weight savings and being compatible with existing lines. With increased production and supportive state policy such as the Uttar Pradesh Bioplastics Policy 2024, the gap is expected to narrow even further.

Why now?

India has already banned 19 categories of single-use plastic, and that compostable claims must be verified by a third-party certification and an IS/ISO171088 credential before any product is commercially available. This leads to a level of trust and a clear direction. As a listed company, BCML also reports environmental data through SEBI’s BRSR with regard to accountability as their business scales. Experts agree, if the policy, scale, and public procurement converge compostables will rapidly move from “nice-to-have”, to standard.

The potential is considerable. India’s current PLA market is around 20,000 tonnes, but demand across cutlery, straws, personal care and food delivery is in the several lakh tonnes. With the right infrastructure and scaling, bio-based packaging can reduce landfill volumes, limit emissions, and enhance India’s position in sustainable manufacturing as the world shifts to greener alternatives. Public pilots like Ayodhya become demonstration sites people see, touch, and trust the alternative. From temple towns to urban kitchens, sugarcane is creating a new chapter of packaging that respects culture and the planet and is built to align with India’s priorities.

Walking outside huge fashion streets and stores in the country and worldwide, it is interesting to see brands that are so intensely associated with overconsumption, starting to introduce sustainability initiatives. Many of them even explicitly ask you to not buy clothes unnecessarily. Millions of discarded clothes end up as waste, piling up in landfills and creating mountains of textile cast-offs. The majority of these items could have been re-worn, reused, or recycled, yet they continue to end up as waste.

This growing issue is putting major retailers under increasing pressure to take meaningful action and implement more responsible waste management practices.

While companies like Adidas and luxury giant Kering — the parent company of brands such as Alexander McQueen and Gucci — have set ambitious targets for collecting used garments, the broader goal is clear: to ramp up textile recycling, keep clothes out of landfills, and give fashion waste a second life.

H&M’s Conscious Collection and Zara’s Join Life line exemplify efforts to incorporate recycled materials and promote circular fashion. Yet, industry observers have made claims that despite these initiatives, both brands continue to face scrutiny over their broader environmental impact and accusations of ‘greenwashing’, raising questions about the authenticity and depth of their sustainability claims.

With glossy catwalks, glitzy trends, and overnight sensations, it’s true that fashion is a world built on constant reinvention. Yet behind the allure of the latest drop lies a deeply frayed system. The global fashion industry, worth a staggering $1.84 trillion and contributing 1.63% to the world’s GDP, is confronting a long-overdue reckoning. As the climate crisis intensifies and consumers demand accountability, fashion must grapple with an uncomfortable truth: its allure comes at an immense environmental and human cost.

The industry alone contributes 8–10% of global carbon emissions—more than all international flights and maritime shipping combined. Each year, it generates 92 million tons of textile waste, with much of it either incinerated or dumped in landfills. A single cotton shirt guzzles over 2,700 litres of water during its production, while the industry as a whole consumes a jaw-dropping 79 trillion litres annually. Then there’s the plastic: synthetic fabrics release over 500,000 tons of microplastics into waterways each year. Compounding this crisis is the grim social reality—an estimated 50 million people are trapped in modern slavery, many within the opaque corners of the fashion supply chain.

But fashion’s unravelling isn’t just a crisis. It is an opportunity. Driven by regulation, consumer demand, and innovation, a systemic transformation is taking root—one that promises to redefine fashion from fibre to finish.

Spotlight on India’s Fashion Industry

In India, one of the world’s largest garment producers and exporters, the fashion supply chain is marked by both promise and peril. The 2024 Fashion Transparency Index flagged major transparency gaps globally—but Indian brands were especially concerning. According to the Advertising Standards Council of India (ASCI), nearly 79% of environmental claims made by Indian brands were either misleading or completely unsubstantiated.

This trust gap is wide: only 29% of Indian consumers say they trust sustainability claims made by fashion brands. That skepticism is well-founded. Investigations by non-profit Transparentem in Madhya Pradesh revealed forced and child labour across 90 cotton farms, with workers exposed to toxic chemicals and bound by exploitative contracts. Despite these abuses, raw material suppliers—especially those in Tier 2 and Tier 3 cities—are rarely disclosed in brand reports, keeping violations hidden from public scrutiny.

This opacity also fuels greenwashing. Just as European regulators struggle to verify the authenticity of “recycled yarns” or eco-labels, India’s regulatory frameworks remain nascent. Brands can still advertise sustainability while dodging genuine accountability.

The World Watches

Globally, governments are raising the bar. The EU is at the forefront, rolling out sweeping reforms like the Ecodesign for Sustainable Products Regulation (ESPR) and the Corporate Sustainability Due Diligence Directive (CSDDD). These policies enforce strict standards on durability, recyclability, and human rights due diligence. Meanwhile, the Digital Product Passport (DPP) will soon require every product to come with a scannable QR code that reveals its environmental impact and supply chain footprint.

The U.S. is not far behind. New York and California have banned PFAS “forever chemicals” in clothing starting 2025, while Extended Producer Responsibility (EPR) laws in states like Oregon and California are shifting waste disposal costs back to the brands. The Uyghur Forced Labor Prevention Act (UFLPA) is also being enforced with greater rigor, underscoring the rising scrutiny on unethical labour practices.

Fashion’s Digital Thread

As policy tightens, technology is stepping in to bridge the compliance gap. Blockchain is revolutionizing traceability by creating tamper-proof records of a product’s journey. Brands like Givenchy and Breitling are already using it to authenticate products and verify ethical sourcing. Artificial Intelligence is being deployed to refine demand forecasting, helping brands slash the overproduction that fuels fashion waste. Over 70% of mass-market design now uses 3D sampling—reducing the need for physical prototypes and cutting time-to-market drastically.

On the recycling front, companies like Circ and Syre (partnering with H&M in a $100 million initiative) are pioneering closed-loop systems to recover and reuse cotton and polyester from discarded clothes. Yet the biggest challenge remains scale. While these breakthroughs are promising, they’re still far from replacing the global supply chain’s vast output.

The Conscious Consumer Is Here to Stay

Fashion’s new power players aren’t designers or CEOs—they’re conscious consumers, especially Gen Z. A remarkable 73% of Gen Z buyers say they’re willing to pay more for sustainable products. Globally, three out of five shoppers now consider sustainability when making purchasing decisions.

This shift is transforming fashion’s economics. The resale market is booming, growing at 12% annually and poised to represent 10% of global apparel sales by end-2025. Even the popularity of ‘dupes’, the affordable alternatives to luxury products, reflects a rising awareness that value isn’t just about price tags, but also about ethics, craftsmanship, and longevity.

Indian consumers are also leaning into this shift. There’s growing support for small, artisan-driven labels that emphasize fair wages, traditional techniques, and lower environmental footprints. The demand for transparency is turning the spotlight on brands that embrace purpose over profit.

Strategies for a Sustainable Tomorrow

Rebuilding the fashion industry from the ground up demands sweeping reforms. At the heart of this lies radical transparency. Disclosing only Tier 1 suppliers is no longer enough; brands must trace their materials to the farm or mine. Technologies like blockchain and initiatives like the Higg Facility Environmental Module (FEM) are helping brands gather real-time environmental and social data. Movements like Fashion Revolution are amplifying the push for visibility, calling for a new era of open accountability.

Decarbonisation is another key pillar. Since 70% of emissions occur in the early supply chain, investments in renewable energy, regenerative agriculture, and innovations like waterless dyeing are crucial. Brands such as Primark are taking first steps by designing garments to withstand 45+ washes—reducing their water, carbon, and waste footprints by nearly 30%.

A material revolution is also underway. With over 70% of textiles still made from fossil-fuel-derived synthetics, shifting to organic cotton, recycled fibres, and bio-based materials is imperative. Innovations like Mirum (plant-based leather) and Biosteel (biodegradable fibre used by Adidas) hint at a plastic-free future—but scaling them will require major R&D investments.

Circularity, once a buzzword, is fast becoming a business imperative. From design-for-disassembly to large-scale recycling infrastructure and take-back programs, the industry is learning to close the loop. France and Belgium’s EPR laws already compel brands to take responsibility for a garment’s entire lifecycle. Meanwhile, fast fashion giant Inditex is working with Ambercycle to scale up recycled polyester production.

None of this will work without ethical labour practices. Ensuring safe conditions and living wages—especially among invisible Tier 2 and Tier 3 suppliers—is not optional. Brands must go beyond audits, setting wage benchmarks and forging binding agreements. While “nearshoring” and “friendshoring” (producing closer to home or in politically friendly regions) are gaining ground, they introduce new challenges in capacity and cost.

🌏 Fashion Sustainability & Greenwashing: India vs Europe (2024 Snapshot)

| Category | India | Europe |

| Sustainability Claims Accuracy | 79% of green claims are exaggerated or misleading (ASCI) | 59% of claims found to be vague or unverifiable (EU Commission) |

| Consumer Trust | Only 29% of consumers trust sustainability claims (ASCI) | Around 44% consumer trust in major European countries (EU Survey 2023) |

| Raw Material Supplier Disclosure | Very limited, <5% brands disclose Tier 2/3 suppliers (Transparentem) | Only 5% disclose raw material suppliers (Fashion Transparency Index) |

| Labour & Environmental Violations | 90 cotton farms in Madhya Pradesh found using forced & child labor | Labour exploitation mostly in outsourced supply chains (e.g., Bangladesh) |

| Government Regulation | ASCI Guidelines against greenwashing launched mid-2023 | EU Green Claims Directive introduced to standardize & verify claims |

| Focus of Activism & Scrutiny | Waste management, labour rights, textile waste | Fast fashion emissions, synthetic fibers, microplastics |

The Road Ahead

The path to sustainability is expensive, complex, and slow. Experts estimate that the global industry needs more than $1 trillion in investment to hit its sustainability targets. Smaller brands, which make up over 90% of the sector, often lack access to capital, technology, or certified suppliers. Fragmented global supply chains and the lack of standardised data make it hard to benchmark progress.

Still, the pressure to change is mounting. Regulatory frameworks like the EU’s Digital Product Passport and India’s evolving EPR policy are setting new norms. The climate clock is ticking, and brands that delay may find themselves left behind—not just in compliance, but in relevance.

The fashion industry, long defined by speed and spectacle, is learning to slow down and stitch purpose into its seams. A new era is unfolding—one that redefines success not by runway applause, but by impact, responsibility, and resilience.

The gleaming solar farms stretching toward the horizon and the silent glide of electric vehicles on city streets are the visible icons of our promised sustainable future. Yet, beneath this polished surface lies a far more complex, gritty, and rapidly evolving reality: a profound revolution reshaping the very arteries that deliver green technology, which are its global supply chains. This intricate network, once relegated to the background as a logistical necessity, has surged to the forefront as the critical frontier where the true environmental and social cost of the energy transition is being determined. What was once an afterthought is now recognized as the linchpin for genuine sustainability, driving an unprecedented, multifaceted transformation that is as challenging as it is essential for the future of both the planet and the clean tech industry itself.

Mounting climate catastrophe demands drastic reductions in greenhouse gas emissions across the entire value chain, far beyond a company’s direct operations. Scope 3 emissions, encompassing everything from raw material extraction and processing to manufacturing, transportation, and end-of-life management, often constitute a crushing 70-90% of a green tech company’s total carbon footprint, according to comprehensive analyses by organizations like CDP. Simultaneously, governments are wielding regulatory power like never before. The European Union’s Carbon Border Adjustment Mechanism (CBAM), imposing carbon costs on imports of steel, aluminum, cement, fertilizers, electricity, and hydrogen starting its transitional phase in October 2023, fundamentally alters the calculus for global suppliers. The EU Battery Regulation, fully effective since February 2024, mandates rigorous carbon footprint declarations, performance and durability standards, and escalating targets for recycled content in lithium, cobalt, lead, and nickel used in batteries – a direct assault on the environmental impact of this crucial green tech component. This regulatory tsunami is echoed globally, from US incentives tied to domestic sourcing and labor standards to emerging frameworks in Asia.

Adding immense pressure is the insatiable demand for critical minerals – the lifeblood of batteries, permanent magnets in wind turbines, and advanced electronics. The International Energy Agency (IEA) projects that overall demand for critical minerals could triple by 2030, with lithium demand alone potentially increasing by over 40 times by 2040 under net-zero scenarios. This voracious appetite collides with the harsh reality that securing these resources is impossible without addressing the ethical and environmental scandals that have plagued mining: child labor in cobalt artisanal mines in the Democratic Republic of Congo, devastating water pollution from lithium extraction in South America, and land rights conflicts globally. Ethically conscious consumers, empowered investors wielding trillions in ESG-focused capital, and advocacy groups are demanding radical transparency and accountability, making unsustainable sourcing not just unethical but a severe reputational and financial liability. The revolution, therefore, is not merely desirable; it’s a fundamental requirement for securing the resources needed for the energy transition itself.

This supply chain metamorphosis manifests in profound and diverse ways across every link. At the source, mining giants face unprecedented pressure to adopt and adhere to stringent environmental and social standards. Frameworks like the Initiative for Responsible Mining Assurance (IRMA) are moving from aspirational to essential benchmarks. Pioneering companies are forging new paths: BMW secured the world’s first supply contract for carbon-reduced steel produced using green hydrogen from Sweden’s H2 Green Steel, aiming for near-zero emissions. Apple, a major consumer of cobalt for batteries, has committed to using 100% recycled cobalt in all Apple-designed batteries by 2025 and is actively auditing its supply chains down to the smelter level. The quest extends beyond recycling to innovative extraction methods like Direct Lithium Extraction (DLE), which promises significantly lower water usage and land impact than traditional evaporation ponds.

The journey of materials, which is the logistics spine, is undergoing its own radical decarbonization. Shipping, responsible for nearly 3% of global CO2 emissions, is a major target. Maersk’s bold investment in a fleet of dual-fuel container ships capable of running on green methanol represents a significant bet on alternative fuels, though scaling production remains a hurdle. Companies are leveraging artificial intelligence for sophisticated route optimization, significantly slashing fuel consumption and emissions across road, sea, and air freight. Simultaneously, the push for Sustainable Aviation Fuels (SAF) is intensifying, driven by corporate commitments to reduce supply chain emissions, though cost and availability are still significant barriers. The focus is shifting from mere efficiency to genuine decarbonization of movement.

Perhaps the most fundamental shift is the rise of the circular economy from a niche concept to a core operational necessity. The linear “take-make-dispose” model is untenable for resource-intensive green tech. Innovations in battery recycling are leading this charge. Companies like Redwood Materials, founded by Tesla co-founder JB Straubel, and Li-Cycle are developing advanced hydrometallurgical and mechanical processes aiming to recover over 95% of critical metals like lithium, cobalt, and nickel from end-of-life batteries and manufacturing scrap. This contrasts starkly with the Global Battery Alliance’s estimate that currently less than 5% of lithium-ion batteries are recycled globally, highlighting both the immense challenge and opportunity. Beyond batteries, designing products for disassembly, implementing robust take-back schemes, and establishing industrial-scale recycling for solar panels (which face a potential tsunami of waste as early deployments reach end-of-life) and wind turbine blades are critical priorities. The goal is clear: transform waste streams back into valuable feedstock, drastically reducing the need for virgin mining and its associated impacts.

Underpinning all these efforts is the rising demand for radical transparency. Gone are the days of vague sustainability promises. Blockchain technology, piloted by companies like IBM (Food Trust, now part of the IBM Environmental Intelligence Suite) and MineHub Technologies, is being explored to create immutable ledgers tracking materials from mine to final product. Comprehensive Life Cycle Assessments (LCAs) are becoming standard practice, quantifying environmental impacts across the entire product lifespan. This transparency allows companies like Patagonia (with its Footprint Chronicles) and Tesla (increasingly pressured to disclose its battery mineral sourcing) to validate their sustainability claims and empowers consumers and investors to make informed choices. Crucially, it also exposes greenwashing, holding companies accountable for their entire value chain impact.

Despite the undeniable momentum, the path is fraught with formidable hurdles. Transitioning to sustainable supply chains often carries higher initial costs for materials, logistics, and compliance. Engaging and auditing complex, multi-tiered supplier networks, often operating in regions with limited oversight, remains a herculean task. Technological limitations persist, particularly in efficiently recycling complex products and scaling green hydrogen or SAF production. Persistent gaps in global standards and verification mechanisms create confusion and loopholes. Geopolitical tensions and trade policies add another layer of complexity to securing resilient and responsible supply chains.

Yet, the trajectory is clear and irreversible. The plummeting cost of renewable energy is making green manufacturing increasingly viable. The reputational and financial risks of unsustainable practices are too great to ignore. Most fundamentally, there is a dawning, industry-wide realization: a genuinely sustainable future powered by green technology is impossible without green supply chains. The revolution transforming these once-hidden networks is no longer merely an ethical choice; it has become the indispensable bedrock of competitive resilience, resource security, and ultimately, planetary survival.

The e-commerce giant achieved a major sustainability milestone in 2024, delivering 1.5 billion packages via electric vehicles worldwide – more than doubling its EV fleet to 31,400 units and exceeding its India electrification target a year early. This achievement, detailed in Amazon’s latest Sustainability Report, comes alongside its fifth consecutive year as the world’s top corporate buyer of renewable energy, matching 100% of global operations with clean power.

Balancing Growth with Emissions Reduction

While Amazon’s absolute carbon emissions rose 6% to 68.25 million metric tons due to business expansion, the company highlighted a 40% reduction in carbon intensity since 2019. Key decarbonization efforts included:

AI Efficiency Breakthroughs

Amazon Web Services countered AI’s energy demands with:

Sustainable Operations Expansion

The company made strides across its value chain:

Fresh off announcing India’s largest green hydrogen facility, engineering giant Larsen & Toubro has secured a strategic ultra-mega offshore contract in the Middle East, showcasing its unique dual capability in traditional hydrocarbons and clean energy transition.

The company’s hydrocarbon division landed a major EPCI (engineering, procurement, construction, installation) contract involving new offshore structures and facility upgrades, continuing its three-decade legacy of executing complex oil and gas projects across water depths. “This award reinforces our global reputation for delivering technically challenging offshore projects with precision,” L&T stated, highlighting its in-house engineering expertise and specialized marine fleet.

Simultaneously, L&T Energy GreenTech is pioneering India’s energy future through its 10,000-tonne annual capacity green hydrogen plant at IOCL’s Panipat refinery. The fully renewable-powered facility will employ indigenously manufactured alkaline electrolyzers from L&T’s Hazira unit, supporting India’s green hydrogen mission while decarbonizing hard-to-abate sectors.

“This parallel execution of hydrocarbon and clean energy projects demonstrates our balanced energy transition approach,” said Subramanian Sarma, L&T’s deputy MD. The twin developments position L&T as both a global hydrocarbon infrastructure leader and domestic clean energy champion – a rare combination in today’s polarized energy landscape. The green hydrogen facility, operating on a 25-year BOO model, represents one of India’s first industrial-scale implementations of the National Green Hydrogen Mission, while the Middle East contract extends L&T’s dominance in conventional energy infrastructure amid growing global energy demand.

A promising innovation in green construction is emerging from Bengaluru’s Indian Institute of Science. Novacret, a startup incubated at the Foundation for Science, Innovation and Development (FSID), is set to launch its revolutionary green cement product by September 2025. The product boasts up to 80% lower carbon emissions and eliminates the need for water during curing, making it both eco-friendly and water-efficient. Rooted in circular economy principles, Novacret uses industrial waste—including fly ash from power plants and slag from steel industries—as raw materials, drastically cutting environmental impact while offering a cost advantage.

The performance metrics of Novacret are compelling. Unlike conventional concrete, which typically takes 28 days to reach full strength, Novacret products achieve the same in just three days. Additionally, they are currently 10–15% cheaper than traditional concrete offerings, and the cost is expected to drop further with scale. Its product line includes a wide variety of precast items such as pavers, kerbstones, AAC blocks, CLC panels, facades, and porous pavers—all packaged in innovative compostable bags to minimize plastic waste.

The startup has already attracted interest from major players in the real estate and infrastructure sector, including pilot projects with large construction firms and potential collaborations with the Karnataka government. Novacret also plans to incorporate agricultural waste into its production in the coming years, which could have a significant impact on reducing stubble burning and air pollution in northern India. This could further boost India’s climate targets under global frameworks like the Paris Agreement.

Internationally, Novacret is eyeing partnerships in Dubai, Abu Dhabi, and Sharjah. It recently showcased its technology at the World Future Energy Summit 2025 in Abu Dhabi and was among 12 startups featured at India’s Construction Tech Demo Day. Backed by grants from the Department of Science and Technology and Zerodha CSR, the startup is now preparing for its first seed funding round to support its next stage of growth.

Novacret’s broader vision aligns closely with the concept of “Drawdown,” a framework proposed by Paul Hawken for reversing global warming within a generation. With construction accounting for over 25% of global carbon emissions, Novacret offers a viable, scalable path for decarbonising the sector. The startup estimates that the market potential for its products in India exceeds $1 billion, with engineering blocks alone worth $1.3 billion. Globally, the precast concrete market is pegged at $166 billion, and Novacret aims to capture at least 10% of that within the next five years. By converting industrial and agricultural waste into high-performance construction material, Novacret is more than just a green cement startup—it represents a blueprint for sustainable urban development. If adopted at scale, it could slash the construction industry’s carbon footprint by half within a decade, delivering tangible climate action from the ground up.

The Sustainability Mafia (SusMafia), a 100+ strong network of climate-tech pioneers, has unveiled its ‘Climate-Tech Opportunity Map’ – a curated guide spotlighting 25 high-potential ideas to slash India’s carbon footprint. This actionable blueprint targets critical gaps in energy, agriculture, industry and water sectors, combining emissions data with expert insights to highlight scalable solutions.

Developed under SusMafia’s SusVentures program, the initiative connects aspiring entrepreneurs with mentors, investors and pilot partners. “We’re helping climate builders validate ideas faster and access the right networks,” explains Aneesa Patel, SusVentures Co-Founder. The map’s co-creators emphasize its mission: “India needs startups solving the right problems urgently – this bridges the gap between pressing challenges and entrepreneurial action.” By focusing on underserved markets with clear white spaces, the map aims to accelerate viable climate solutions from ideation to market impact.

Copyright © 2026 Green Trendsetters. Terms of use. Privacy policy.